Understanding the Difference Between APR and APY

Difference Between APR and APY

When navigating the world of personal finance, you’ll often encounter the terms APR (Annual Percentage Rate) and APY (Annual Percentage Yield). Both are critical in understanding the true cost of borrowing and the potential returns on savings, but they serve different purposes and are calculated differently. Here’s a closer look at how APR and APY compare, and why understanding both is essential for making informed financial decisions.

What is APR?

APR (Annual Percentage Rate) is a measure used to express the yearly cost of borrowing money. It includes not just the interest rate, but also any other fees or costs associated with taking out a loan, such as origination fees or closing costs. APR is most commonly associated with loans and credit cards, and it gives you a more accurate picture of what you’ll pay over the life of the loan.

Key Points about APR:

- Usage: Used to describe the cost of borrowing money, primarily in loans and credit cards.

- Components: Includes the interest rate plus other fees or costs.

- Purpose: Helps borrowers understand the true cost of a loan.

What is APY?

APY (Annual Percentage Yield), on the other hand, reflects the actual rate of return earned on savings or investments over a year, accounting for the effects of compounding interest. Unlike APR, which is focused on costs, APY is concerned with earnings, and it provides a more accurate representation of your investment growth by including how often interest is compounded.

Key Points about APY:

- Usage: Used to describe the potential earnings on savings and investment accounts.

- Components: Includes the interest rate and the frequency of compounding.

- Purpose: Helps savers understand the real return on their investments.

How Are They Calculated?

- APR Calculation: APR is calculated by taking the total cost of borrowing (interest plus fees) and expressing it as an annual rate. It does not consider the compounding of interest.

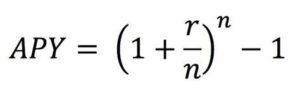

- APY Calculation: APY takes the nominal interest rate and factors in how often the interest is compounded within a year. The formula for APY is:where r is the nominal interest rate and n is the number of compounding periods per year.

Hypothetical Scenario for Comparison

Imagine you’re comparing a credit card and a savings account:

- Credit Card (APR): You have a credit card with an APR of 18%. This means that over the course of a year, if you carried a balance, you would pay 18% of that balance in interest, assuming no additional fees or changes in the balance.

- Savings Account (APY): On the other hand, you’re considering a savings account that offers an APY of 2%, compounded monthly. This means that over a year, you’ll earn 2% on your savings, but because of monthly compounding, the actual interest earned will be slightly higher than 2% of your initial deposit.

If you deposit $1,000 in the savings account, you will have more than $1,020 by the end of the year because of the compounding effect.

Key Differences

- Purpose: APR is designed to help borrowers understand the total cost of a loan, while APY is meant to show savers the real return on their deposits.

- Compounding: APR does not account for the effects of compounding, while APY includes compounding in its calculation.

- Cost vs. Earnings: APR focuses on what you’ll pay, and APY focuses on what you’ll earn.

Why Understanding Both Matters

Knowing the difference between APR and APY is crucial for making smart financial decisions. If you’re borrowing money, understanding APR helps you compare the true costs of loans. If you’re saving or investing, knowing APY helps you identify the accounts that will maximize your returns.

By understanding how APR and APY are calculated and what they represent, you can better compare financial products and make decisions that align with your financial goals.